If you have ever had the experience of running a pro shop or restaurant operation, you would know that understanding and dealing with payment processing is an incredibly complicated process. Getting set up to simply take credit card payments requires mental gymnastics to understand fees, processors, providers, interchange rates, payment models, and something called an ISO.

It can seem like getting a fair deal requires a PhD or you’ll end up getting screwed by some greasy used car salesman. We want to help you get a fair deal and that starts with clarifying this increasingly confusing side of running a business. So, without further ado here’s how payment processing works at golf courses.

What Are Payment Providers, Processors, and ISO’s?

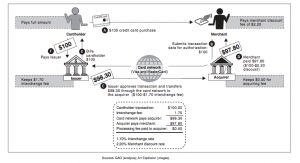

As a basic rule, when a customer pays with their credit card at your golf course, a fee will be taken from the amount paid and given to the payment processor. You heard me correctly, those vacation points customers get from using those premium cards are paid for by you.

Of course, we’re talking about a small percentage on each transaction, but these transaction fees add up quickly. We’ll go over some strategies to get a better deal later on in this article, but we’ll start by going over how these fees actually work.

Once payment is taken by a payment processor, the processor pays a fee to the credit card provider (like Visa or MasterCard). This fee that is charged by the credit providers to the processors is called the interchange fee. The interchange fee for each credit card is typically factored into the processing fees used by the processors and is ultimately charged to the merchant (you).

Since interchange fees vary from card to card, there are several models processors use to set up their processing fees:

- Interchange plus

- Fixed rate

- Fixed rate barter

- Cash discount

So, let’s break down each processor fee model.

The Interchange Plus Model

This is the most common model found across retail businesses that take payments through a POS system. In this model, the payment processor charges the merchant for whatever the credit card provider’s interchange rate is, plus an extra provider fee. This provider fee can either be a percentage, a fixed charge (20 cents for example), or the additional charge may fluctuate to whichever is greatest between the fixed charge or the percentage.

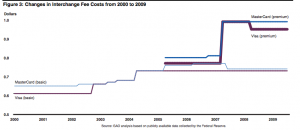

The reason so many businesses choose this model is that interchange rates in the United States vary from card to card and can fluctuate from .9% to 3.25%. If most of your credit card using customers paid with low interchange rate cards it make sense to go with this model over a fixed rate model. However, today 92% of all credit card transactions are paid on premium rewards cards that typically feature higher interchange rates. To make things worse, interchange rates have increased by 68% since 2008 and are only expected to increase.

The best option really depends on the average interchange rate found between credit cards used at your business. This can be calculated by taking your total credit card volume and dividing it by total cost over the course of a month. By our own calculations, the average interchange rate between all credit card types is 2.4%.

Pros:

- Most commonly found

- Flexibility in choice of processors

- Not locked into an unfair rate

Cons:

- Businesses are forced to honor all cards

- Interchange rates are trending upwards

- Interchange for premium cards exceed fixed rates

The Fixed Rate Model

To fight back against ever increasing interchange rates, many processors and business are beginning to move towards the fixed-rate model. Under this model, businesses and processors get some leverage against the problems that come with fluctuating interchange rates.

The fixed rate model essentially says “since interchange rates fluctuate, I’ll benefit more in the long run by sticking with a median fixed rate that won’t fluctuate”.

In this model, the processor chooses to charge a flat rate, for example 2.2%, and absorb the interchange fees charged by premium cards, while benefiting from cards with lower interchange rates.

Chances are pretty strong that the majority of your clientele use premium cards with higher interchange rates like American Express or Visa Aventura. So, knowing this, it may be a better choice to go with a fixed rate.

Pros:

- The fixed rate is typically below the average interchange fee

- No requirement to pay high interchange rates for premium cards

- Flexibility to accept all cards at a lower cost

Cons:

- Forced to pay a higher rate for low interchange rate cards

- Less flexibility to get a better rate

- Limited choice of payment processors

The Fixed Rate Barter Model

This model is an extension of the fixed rate model. Instead of paying for your software in fixed monthly payments or with bartered tee times, you pay for management software through a higher fixed rate processing fee.

For example, instead of paying 2.5% per transaction in a fixed model and then monthly fees on top of that for your management software, you could instead pay 4% for each transaction. The 2.5% would still go to the provider, but the software company would then receive the remaining 1.5%.

This can simplify paying for management software, and it works well for seasonal businesses that see demand fluctuate month to month.

Smaller operators called Independent Sales Organizations (ISO’s) tend to operate in this space. Typically these processors will partner with golf management software companies to provide a fair rate since the management software companies have more leverage over these smaller ISO’s and are able to provide a large account.

Pros:

- Simplify the process of paying for software

- Pay for software only by doing business

- Effective for seasonal markets

- More leverage on the processing companies

Cons:

- Risk of overpaying for software

- Some service providers take days to send funds to your account

The Cash Discount Model

The last way of dealing with payment processing fees is to implement a cash discount model. This model is used for operators that charge a fee directly to the customer when they use a credit card, or discount any payment made in cash.

Implementing this model is very simple, especially if your POS system makes it easy to add a cash discount button to the terminal. This model completely passes on the cost of payment processing to the customer and encourages them to pay only with cash.

This model can be very effective in many situations, especially ones where speed and simplicity of payment are highly valued, like in a snack cart situation. However, there are some obvious downsides.

Credit card use is only increasing so this model risks alienating customers who prefer to pay by credit. Limiting customers who only pay by card by requiring them to pay more may be damaging to their experience and could even result in lost business if they don’t carry cash. Additionally, from a legal standpoint, you need to be careful when implementing this technology since laws regarding fees charged directly to the customer vary by country, province, and state.

Pros:

- Eliminate payment processing costs

- A simple strategy to circumvent the system

- Low cost to implement

- No negotiation with processors necessary

Cons:

- Risk of frustrating customers with extra fees

- Not legal in all countries, states or provinces

- Increased price sensitivity

- Still required to invest in payment processing hardware

- Difficult to implement online

Our advice for getting a good deal

By now, I hope that the different models in the world of payments and processing are a little bit clearer. You’re probably still asking yourself: “How can I can get the best deal?”

How to get a good deal:

- Shop around

- Negotiate your hardware and rate

- Know how your rate works before negotiating

- Understand why you might be paying extra fees

- Be aware of the laws and regulations in your region

How should I shop around?

The good news is that you do have some degree of leverage over your processing partners. For them to exist, they need you to exist . Golf courses represent a low-risk category for them, so ultimately they will want your business. Play your cards right with good negotiation tactics. Pit competing processors against one another and you could end up in a race to zero. You have the right to negotiate for a better rate and a lower hardware cost.

Your best bet is to get a quote from a variety of processors. Investigating the rates you can get for each model between processors is likely to provide insights about which payments model is best for you. Since not all payment processors are created equal you’ll need to understand how each one will treat your business.

Here’s a list of processors that should be on your list:

- Moneris

- Chase Paymentech

- Heartland Payment Systems

- Stripe

- Elavon

- Vantiv

- TSYS

- WorldPay

- Global Payments

What should I know before negotiating?

Knowing your existing rate before looking at a switch is incredibly valuable for negotiating a new deal. Call up your provider and ask them to give a clear breakdown of what you are paying. This might involve doing some analysis to uncover any hidden fees that your processor doesn’t include in their quoted rate. You can calculate this rate by dividing total volume by total cost for the month.

Once you know your actual rate you can enter negotiations with a strong hand. If you get a good quote, leverage it with your existing provider. Play hardball between your options, based on our past experiences these companies are not afraid to undercut each other’s prices, so don’t be afraid to instigate a small bidding war to earn your business.

Hardware in this business is almost a commodity, in some cases, you can negotiate a deal that will get you PIN pads for free. Consider bringing this subject up with a prospective payments partner, they may be able to get you a very low price.

If you calculate your “real” rate as discussed earlier, you may be shocked to discover that the fees you pay are much greater than you previously expected. There are many possible reasons for that, but two of them might be:

- Payment gateway services

- Card not present fees

What is a payment gateway?

A payment gateway is typically used when the software you use to process payments is not directly integrated with your payment processor. Wait… what? I thought the software I use was integrated! What’s going on?

Chances are your software is integrated with a payment gateway, and that payment gateway integrates with your payment processor. Yes, payment gateway providers are yet another middleman in this ever confusing world of payments.

If you are using a payment processor that requires a payment gateway, you are paying a fee to both your payment processor and the payment gateway on every transaction.

Some popular payment gateways that connect 100s of Independent Sales Organizations (ISOs) to the much smaller number of acquirers and processors that integrate with software

- Cayan

- Shift4

- Authorize.net

If you use a payment gateway with your payment processor, its best to perform a cost-benefit analysis. Perhaps you are getting such a good rate from your payment processor that the additional fees to use the payment gateway charges are negligible. Ultimately, if you are stuck with a payment processor and are inflexible to change to a new one, you are going to be charged payment gateway fees. Gateway fees will vary between the various providers, but you will typically pay $0.05 per transaction and some sort of monthly fee.

Card Not Present fees

The second reason you might be charged additional fees is if you are processing a lot of transactions where the card is not present. Typically these transactions refer to online payments, where no physical card is ever used and the customer is only required to enter their information.

Payment processors and credit providers tend to charge an additional fee to cover the extra security risks that come with this kind of transaction.

Now, if you think your golf course is not processing a lot of transactions online, think again. Do you have a member billing cycle? Do you take reservations for tee times online? Do you have an E-Commerce store? If you answered yes to any of these questions then you are in fact paying Card Not Present fees.

One way to get around the Card Not Present fee is to instead use ACH bank drafts instead of credit cards for member billing. Because ACH bank drafts debit charges directly to the account, there’s no need for any card to be involved, thus eliminating the Card Not Present fee. Member billing represents a big chunk of your yearly revenue, so you can save a lot of money in fees by simply requiring customers to use ACH bank drafts.

Unfortunately, this strategy is difficult to apply to E-Commerce and online payments for tee times since ACH bank drafts are somewhat arduous for these smaller transactions. The good news is that amount of revenue you will generate with online booking and e-Commerce quickly outweighs the fractional costs of paying Card Not Present fees.

Payment laws vary from country to country

The rules regarding payment processing vary to a great degree between the USA, Canada Europe,, and the rest of the world. Being aware of compliances rules and local laws will help you avoid fines and penalties charged by credit-card providers, and ensure that you are not breaching any laws designed to protect consumers.

Payment regulations in the USA

In the United States, merchants must be PCI compliant and adhere to the standards and laws enforced by the Federal Government and its Treasury Department.

PCI is the regulatory framework that governs the payment services industry. The framework is set up and defined by Payment Card Industry Data Security Standard (or PCI DSS), a set of standards established by credit providers such as Visa, American Express, and MasterCard.

There are four levels of compliance, but most golf courses fit into the fourth level, which is designed for small businesses that do less than 20,000 credit card transactions per year.

Level 4 businesses must each complete an annual risk assessment and quarterly PCI scans. The risk assessment requires business owners to demonstrate that payment security guidelines are respected. This involves adherence to access controls, network security, data protection, and vulnerability management.

For level 4 businesses there are three ways to validate PCI compliance:

- Externally with a Qualified Security Assessor (QSA)

- Internally with a qualified Internal Security Assessor (ISA)

- Or self-reported through a Self-Assement Questionnaire (SAQ)

The easiest way to validate compliance is through the Self-Assessment, most small businesses choose this route. Submitting an SAQ requires filling out a set of questions and submitting them to the transaction bank. In the event that the answer “no” is given on a SAQ, the merchant must provide an implementation plan to resolve the issue.

Payment laws in Europe

European payment rules are governed by the Payment Services Directive or PSD 2.

In 2009 the EU’s first Payment Services Directive was implemented across all European Union countries. This year, the new Payment Services Directive (PSD 2) will supplement security needs and new developments in payment technology with new regulations. It will be rolled out through 2019.

The PSD contains two sections, one pertaining to the processing companies, and one pertaining to business conduct (including you the merchant). In the business conduct rules section, rules are outlined for liability in case of unauthorized use, and fee transparency requirements. As well, guidelines on how to properly process, refund and revoke payments.

With PSD 2 being rolled out in 2019, amendments to the original PSD will be added that include three major changes for retailers:

- Increased innovation through Access-to-Acounts (XS2A)

- Enhanced security features through Strong Customer Authentication (SCA)

- A ban on surcharging

Access-to-accounts or XS2A will give merchants the ability to directly access consumer bank accounts, with the consumer’s consent. These new rules will make bank transfers for payments much more simple. Consumers will now have the option to pay through means other than credit, and merchants will benefit from lower processing fees and chargeback risk. As well, direct access to bank accounts will make better consumer data analysis possible for retailers.

Strong Customer Authentication or SCA is designed to ensure heightened security at the point of sale, to reduce fraud and theft. From September 2019, in the EU, two-factor authentication will be required for all payments. Authentication methods may be provided via three means:

- Knowledge: a password or PIN code

- Possession: a card or mobile phone

- Inherence: a biometric such as a fingerprint

Since customers value the ease and efficiency of frictionless payment, not all transactions will require two-factor authentication:

- Trusted beneficiaries: the consumer will have the freedom to deem merchants trustworthy, removing the need for SCA.

- Recurring transactions: SCA will only be required for the first transaction if the same payment regularly recurs with the merchant.

- Low-value transactions: Any transaction under 3o euros will not require SCA.

- Low-risk transactions: Transactions that have undergone real-time assessment may be processed without SCA.

For European retailers biometrics may begin to play an increasingly important role for secure payment processing. Retailers will soon be expected to process mobile phone payments given the increased used of biometric measurement in modern smartphones.

Finally, PSD 2 will place a full ban on surcharging for all credit card, debit card, and prepaid card charges. Retailers will no longer be allowed to add extra surprise fees at the cash register. This means the cash discount payments model used by some golf courses will not be permitted in EU countries.

Payment Processing For Golf Courses: Key Takeaways

Payments are the lifeblood of your operation. To remain viable, you must take them every day. So, it’s critical to make sure your methods of taking payments are reliable, secure, efficient, and beneficial for your business.

Payment processors provide a valuable service, but it’s important for the success of your operation to not be exploited by them. Luckily there are ways to leverage providers for a better deal, and there are a variety of payment processing models that suit a variety of needs and situations.

If you plan on negotiating a new deal with a payment processor, make sure to do your research beforehand. Shop around, get a clear idea of what you are currently paying, and don’t be afraid to negotiate for a better rate or a deal on hardware. Get a better deal by knowing your current situation and needs before going into a negotiation.

There may be ways to reduce the costs of paying fees for gateway providers and Card Not Present transactions. Ask your software provider if there is a payment processor that integrates directly with their system so you don’t have to pay gateway provider fees. To reduce Card Not Present fees, choose member management software that permits ACH bank drafts, so you can migrate member billing away from credit card transactions.

A lot has changed in the payment industry and you need to be on top of these changes to ensure the continued success of your business. Make sure to stay up to date with changes to laws and regulations in your region to avoid paying penalties or fines.

Chronogolf now integrates with Lightspeed Payments*, a payment processing platform that provides in-depth tracking so you can know exactly what you are paying. This fixed rate payment processing model has fair rates and comes with detailed reporting to track everything about the payments you take. Learn more about Lightspeed Payments here.

*Only available in the United States.

News you care about. Tips you can use.

Everything your business needs to grow, delivered straight to your inbox.